Drive south out of Dubai on the E11 toward Abu Dhabi and within forty minutes the city begins to thin. The high-rises give way to low industrial sheds, then to bare desert punctuated by date palms and the occasional camel crossing. Then, almost without warning, a different kind of building begins to rise from the sand: long, white, surgically clean, set behind perimeter walls and chain-link fences, with rooftop air-handling units catching the sun and an outdoor switchyard humming quietly at the southern boundary.

This is the spine of the UAE's hyperscaler corridor. It runs along the Dubai–Abu Dhabi axis, dips into Sharjah's free zones to the north, and is now extending west toward the Ruwais industrial belt. In the last twenty-four months it has gone from being a regional curiosity — a place where Microsoft, Oracle, and a handful of regional players had landed — to one of the most actively built hyperscaler markets on earth. The reason is not climate. Cooling a data centre in a 50 °C summer is a problem, not an advantage. The reason is power, and specifically the speed with which power can be delivered.

In Loudoun County, a new 200 MW campus quotes a 2030 energisation date. In west London, a similar campus is in the queue until 2032. In Dubai, the same 200 MW request, made today to DEWA, is typically being quoted at eighteen to thirty months to first energisation. The buildings can keep up. The transformers can keep up. The grid, remarkably for a region not historically associated with industrial electricity, can keep up.

How the Gulf Got Here

The UAE's grid was overbuilt for a long time. Through the 2000s and 2010s, generation capacity was added in step with desalination — the Gulf's water and electricity systems are physically interlocked, with most thermal stations operating as combined water-and-power plants — and the result was a 400 kV transmission system that, by the early 2020s, had spare margin in every major load centre. Dubai's peak demand in 2024 sat around 10.7 GW against an installed capacity of nearly 16 GW. Abu Dhabi was similarly comfortable.

That headroom, combined with the GCC Interconnection Authority (GCCIA) tie that links the six Gulf grids into a single synchronous system at 400 kV, gave the UAE something American and European hyperscalers had stopped finding at home: a grid that could absorb a new gigawatt of load without first reinforcing transmission.

The second piece is institutional. DEWA in Dubai and TRANSCO in Abu Dhabi are vertically integrated, state-owned, and operate to a planning horizon set by the federal government. When the UAE Cabinet announced the National AI Strategy 2031 and the subsequent data-centre-friendly amendments to the Federal Electricity Law, the practical effect was that DEWA and TRANSCO were given a mandate to fast-track hyperscaler connections rather than queue them. There is no British-style "first-come, first-served" backlog. There is a planning office, a coordinated load-growth study, and a willingness to bring forward transmission projects when the load case justifies it.

The third piece, less often discussed but central to the story, is industrial. ETS Group and a handful of other regional transformer manufacturers — building in the UAE, Oman, and Saudi Arabia — have over the past decade developed serious capacity for hot-climate, sand-resilient power transformers up to 500 MVA at 400 kV. That means a Dubai hyperscaler campus does not have to compete with European utilities for a slot at a German factory. The iron is being built closer to home, to a specification that already accounts for the local climate.

What a Gulf Hyperscaler Transformer Actually Looks Like

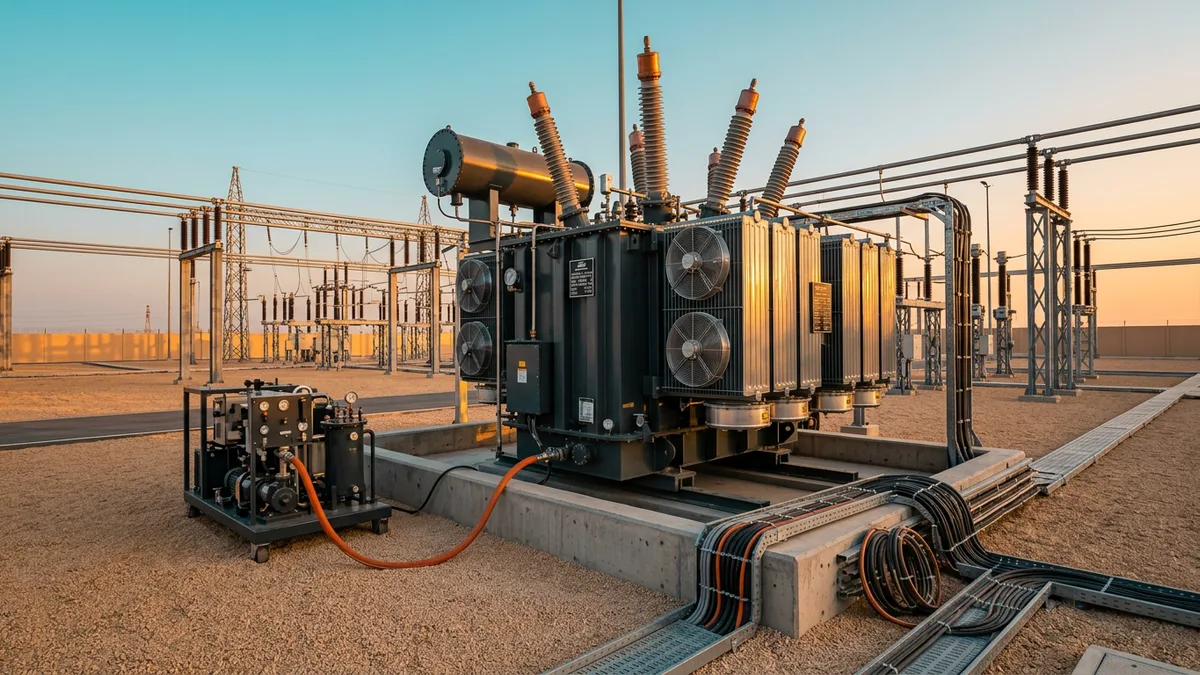

Strip the gloss off a hyperscaler campus in Mohammed Bin Rashid City or KIZAD and you find a substation yard that, at first glance, looks like any other 132 kV or 220 kV transmission yard. Look closer and the local engineering is everywhere.

Cooling first. A standard ONAN/ONAF transformer rated in Europe at 40 °C ambient simply does not deliver its nameplate rating in Dubai in July, where ambient air in the substation yard regularly exceeds 50 °C and tank-top oil temperatures climb correspondingly. The Gulf specification is built around a 50 °C design ambient — sometimes 55 °C for inland sites — with the winding hot-spot, top-oil, and bottom-oil temperature gradients all reworked accordingly. Forced-air radiator banks are oversized, with N+1 fan redundancy as standard, and the ONAF2 rating is the everyday operating point rather than an emergency reserve.

Insulation is the second area of difference. The combination of high ambient temperature, high diurnal swing, and coastal humidity in places like Jebel Ali and Mussafah is unkind to standard mineral oil and to standard cellulose-paper insulation. Gulf hyperscaler transformers are routinely specified with thermally upgraded paper, in some cases with synthetic ester fluid in place of mineral oil for fire-risk-sensitive locations adjacent to IT halls, and with sealed nitrogen-blanket preservation rather than open conservator systems. The result is a transformer designed for a 40-year service life in conditions that would shorten a European unit's life by a decade.

Then sand. Anyone who has walked a substation in the Empty Quarter knows that sand ingress is the silent killer of outdoor electrical equipment. Marshalling kiosks, control cubicles, and on-load tap changer mechanisms all need IP 65 or better. Bushing terminations are commonly cleaned to a higher creepage class than the IEC minimum — typically Class IV (heavily polluted) rather than Class III — to ride through dust storms without flashover. Cable trenches and termination compounds are sealed, and surge arresters are specified with creepage distances that would be exotic in northern Europe.

Finally, the load profile. A hyperscaler in Dubai runs at very high load factor, like its counterparts in Virginia, but the harmonic environment is different. The UPS topology is similar, but the prevalence of large variable-frequency drive loads in adjacent industrial customers — especially in mixed-use free zones — means the primary-side harmonic spectrum the transformer has to live with is richer than in a pure data-centre estate. K-factor 13 with a delta-connected tertiary is a sensible Gulf default.

The Cooling Question, Revisited

The objection to building hyperscalers in the Gulf has always been the same: it is hot, so cooling the IT load must be ruinously expensive. That was true once. It is decreasingly true now.

Two technologies have changed the math. The first is high-temperature chilled water — running the cold loop at 18 to 22 °C rather than the legacy 7 °C, which lets the chillers operate at far higher coefficients of performance and lets the cooling towers reject heat into 45 °C air without losing performance. The second is direct-to-chip liquid cooling for the highest-density AI training racks, where the heat path bypasses room air entirely and the dry coolers on the roof become the dominant heat rejection mechanism.

The combination means that a well-designed Gulf hyperscaler campus today operates at a PUE between 1.30 and 1.40 — higher than a Nordic site, lower than people assume, and competitive with most American markets outside the Pacific Northwest. The electrical penalty of building in the desert is real but no longer prohibitive.

The Money Side

The UAE's hyperscaler boom is not happening in isolation. Saudi Arabia's HUMAIN initiative, the broader Vision 2030 industrial diversification, and the rapid expansion of regional sovereign-cloud capacity have created a flywheel in which the same EPC contractors, the same transformer manufacturers, and the same grid-connection engineering teams are being asked to deliver across multiple GCC markets simultaneously. The Gulf is becoming an integrated hyperscaler supply chain rather than a collection of national markets.

For the UAE specifically, the financial structure that makes this work is the public–private utility model. DEWA's status as a publicly listed company with the Government of Dubai as majority shareholder allows it to raise capital against future tariff revenue at sovereign-adjacent rates, and to do so in tenor matched to the 25-to-40-year life of the transmission assets it builds. American investor-owned utilities cannot match that cost of capital, and British DNOs cannot match the tenor. That difference, more than any planning reform, is what lets the UAE energise a hyperscaler campus in eighteen months.

The Strategic Layer

There is one more thing worth saying, and it is the layer underneath all the engineering. The UAE has decided, at the federal level, that hyperscale compute is strategic infrastructure in the same category as ports, airports, and refineries. That decision has translated into specific instruments — federal-level grid-priority designations, expedited environmental approvals in designated industrial zones, and direct sovereign participation in the equity stacks of several major campuses. None of that is invisible to the hyperscalers when they decide where to put their next gigawatt.

The result is a Gulf hyperscaler market that, in 2026, is not waiting for the grid. It is in many respects the grid — co-designed with the utilities, co-located with the generation, co-procured with the manufacturers, and embedded in a national plan that treats every new megawatt of compute as a contribution to the country's economic diversification.

The buildings will keep rising out of the sand. The transformers will keep arriving from Gulf factories, designed for 50 °C summers and 30-year service lives. And somewhere south of the E11, a switchyard fan will keep turning, quietly doing the work that, in less coordinated parts of the world, is still measured in queue numbers and lead times.